How Much Equity For How Much Money

A dwelling house equity loan is 1 way to tap into your home's worth. Merely since your home is the collateral for an equity loan, failure to repay could put yous at chance of foreclosure. If you're considering taking out a domicile equity loan, hither's what you should know.

What is a home equity loan?

A home equity loan can provide you with greenbacks in the grade of a lump-sum payment that you pay back at a fixed involvement charge per unit, only only if enough disinterestedness is bachelor to you.

Equity is the difference betwixt your domicile's value and what yous still owe on the mortgage. Steadily paying downward your mortgage is one way to grow your domicile disinterestedness . And if real estate values go upward in your expanse, your equity may abound even faster.

How much disinterestedness do you accept?

Your home equity can help you pay for improvements. NerdWallet tin can show you how much is available.

How does a home equity loan work?

A domicile equity loan gives you access to a lump sum of money all at once. If yous know how much money you'll demand and when you'll need it — to finance a remodeling projection with a set budget, for instance — it may exist the right selection.

You'll repay the home disinterestedness loan — principal and interest each month — at a stock-still rate over a prepare number of years. Be sure that you can afford this 2d mortgage payment in addition to your electric current mortgage, as well as your other monthly expenses.

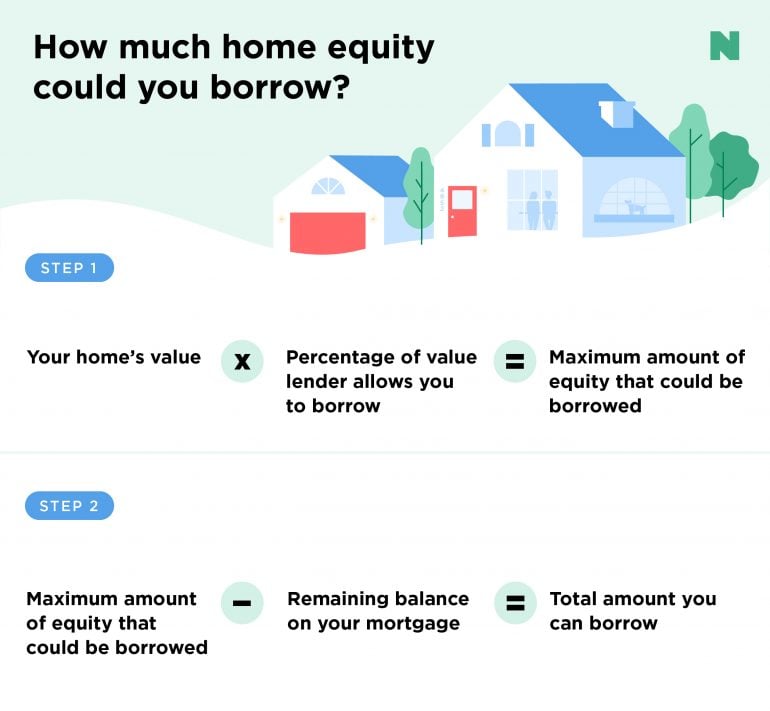

How much tin can you borrow with a home equity loan?

A habitation equity loan mostly allows you lot to borrow around 80% to 85% of your home's value, minus what you owe on your mortgage. You tin can exercise some simple math to approximate how much y'all might be able to infringe.

For example, say your home is worth $350,000, your mortgage balance is $200,000 and your lender will allow you to infringe up to 85% of your habitation's value. Multiply your dwelling's value ($350,000) by the percentage you tin can infringe (85% or .85). That gives you lot a maximum of $297,500 in value that could be borrowed. Subtract the amount remaining on your mortgage ($200,000), and yous'll get the approximate sum you tin borrow every bit a abode equity loan — in this case, $97,500.

Home equity loan requirements

Qualification requirements for home equity loans will vary by lender, simply here's an thought of what you'll probable need in order to get approved:

-

Home disinterestedness of at least 15% to 20%.

-

A credit score of 620 or higher.

In gild to confirm your dwelling house's fair market value, your lender may besides require an appraisal to determine how much you lot're eligible to infringe.

Are home equity loans a adept thought?

Whether a habitation disinterestedness loan is a good idea or not depends on your fiscal situation and what yous programme to practice with the money. Using your home as collateral carries substantial risk, so information technology's worth the time to counterbalance the pros and cons of a home disinterestedness loan.

PROS:

-

Fixed rates provide anticipated payments, which makes budgeting easier.

-

You lot may get a lower interest rate than with a personal loan or credit card.

-

If your current mortgage charge per unit is low, y'all don't have to give that up.

-

If you use the loan for home improvements or renovation, the involvement may be deductible.

CONS:

-

Less flexibility than a abode disinterestedness line of credit.

-

You'll pay interest on the entire loan amount, even if you're using it incrementally, such as for an ongoing remodeling project.

-

As with any loan secured by your house, missed or late payments can put your home in jeopardy.

-

If you make up one's mind to sell your home before you've finished paying dorsum the loan, the balance of your dwelling house equity loan will exist due.

What's the divergence between a abode equity loan and a HELOC?

Unlike the unmarried lump sum of a home equity loan, a domicile equity line of credit, or HELOC , provides flexibility. There'south still a total loan corporeality, but yous only borrow what y'all need, then pay it off and borrow once again. That also ways yous pay back a HELOC incrementally based on the corporeality y'all use rather than on the entire corporeality of the loan, like a credit card.

The other key difference is that HELOCs have adjustable rates . Your charge per unit could rising or fall over the life of the loan, making your payments less predictable. HELOC rates are often discounted at the beginning of the loan. Merely subsequently an introductory stage of around six to 12 months, the interest rate typically goes up.

Source: https://www.nerdwallet.com/article/mortgages/home-equity-loan

Posted by: dewanste1974.blogspot.com

0 Response to "How Much Equity For How Much Money"

Post a Comment